by: Gary Karp

April 30, 2018

Recently, several articles have been published that indicate a renewed momentum in food retailing toward private label share growth. Generally speaking, whether in retail or foodservice, growth in brand share itself is an important key performance indicator (KPI) that impacts other important KPIs.

Recently, several articles have been published that indicate a renewed momentum in food retailing toward private label share growth. Generally speaking, whether in retail or foodservice, growth in brand share itself is an important key performance indicator (KPI) that impacts other important KPIs.

Share shift is reported in retail food channel

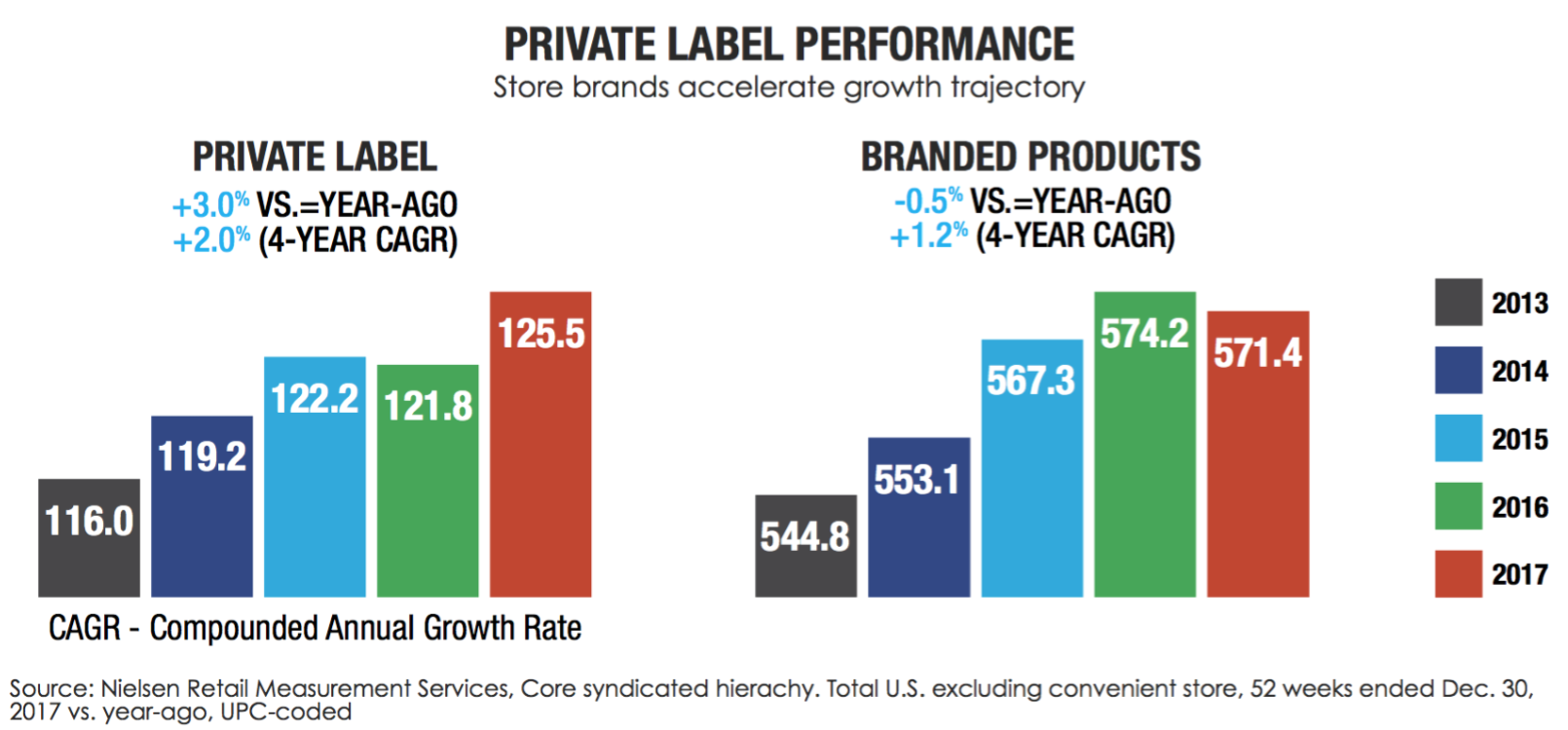

The chart below identifies the growth rate for retail private label and manufacturer brands. A deeper dive in the AC Nielsen Total Consumer Report, provides further insight showing PL growth is led by the premium tier while the discount tier growth has actually slowed.

Foodservice Trading Partners are Seeing Similar Brand Dynamics

Two questions regarding foodservice are:

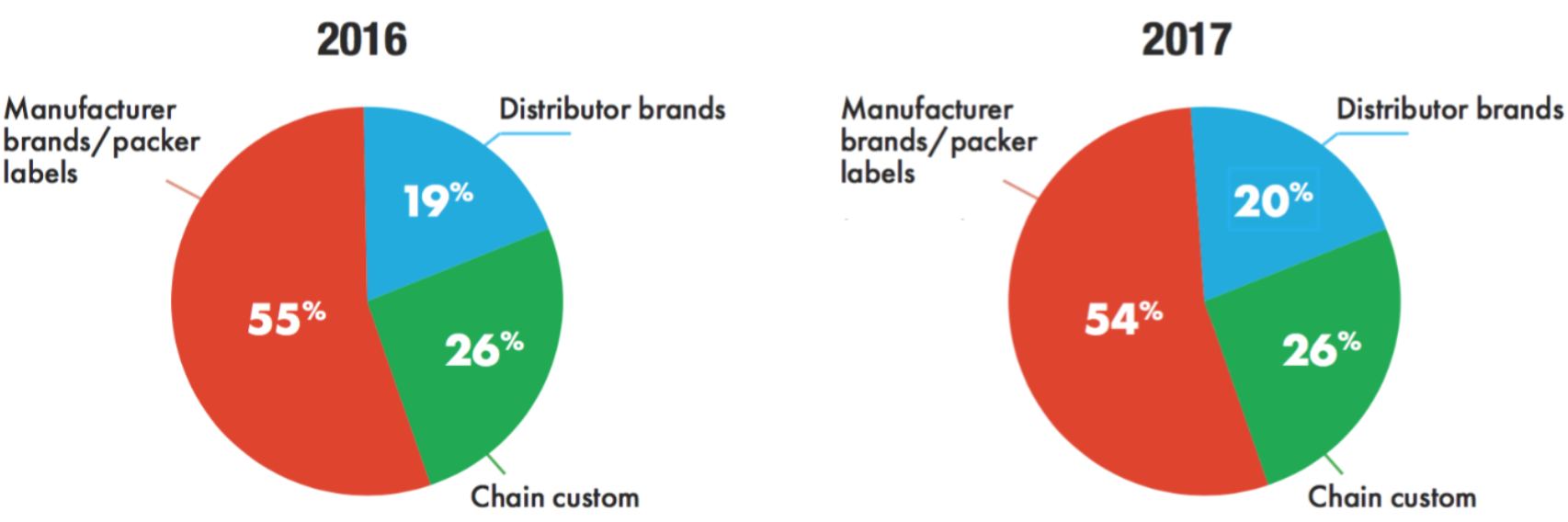

- What are the respective manufacturer, distributor and chain custom brand shares?

- What share changes are likely to happen through 2020?

The Pentallect study, “Go-to-Market 2025: Options and Imperatives” (GTM), answers the first question.

“What are brand shares in foodservice?”

As for the second question, “What share changes are likely to happen through 2020?”

Distributor Initiatives and Results are Evident

Distributors have both motivation and means to grow distributor brands and are increasing their offerings and value proposition on distributor brands.

Two key motivations for distributors to grow their proprietary brands are: First, gross profits per case for private label products are approximately 50-75% higher than they are from typical manufacturer brand products. As a result, a 1% increase in the sales mix could positively impact margins by 9 – 12bp. Secondly, getting customers accustomed to distributor brands should help customer loyalty and continuity. Once they find a brand that works well, FS operators are typically very reluctant to change.

Sysco, in their results reporting on 12/30/17, indicated that for the 26 week period just completed, as a percent of case sales, their US broadline distributor brands was 37.77% and the distributor brand share of local sales was 46%. The sourcing process used by Sysco has, among other initiatives, been a big boost to their distributor brand portfolio.

Recent reports indicate that approximately one-third of US Foods’ revenue comes from distributor brand sales, and US Foods has built up an offering of over 14,000 SKUs across more than 20 brands, and those brands themselves have been segmented into various value tiers.

Further, PFG, in their investor day presentation, has reported that private brands represent 44.6% of independent volume.

In addition, suffice it to say, the other top distributors such as Reinhart, Gordon et al and the distributor co-ops such as UniPro, via their members, are also supporting/seeking distributor label growth.

A Few Basic Recommendations for Trading Partners Looking to Grow Share

As the quality, value proposition and emphasis on distributor brands continues to increase, the challenges for manufacturer brands will continue to grow. Following are some basic, but important recommendations for healthy brands.

- Ensure you have and articulate a viable and demonstrable value proposition.

- Contemporize your brand attributes where possible (ex: sustainable, non-GMO, gluten free, etc.).

- Communicate often what your brand stands for.

- Innovate in product attributes and services including: new products, packaging, supply chain, etc.

- Differentiate to clarify why your brand should be selected.

- Incorporate data analytics to support strategic GTM decisions.

- Enhance direct interaction with key operators. Sales reach and contact quality are critical to drive brand sales.

Brand share is and will continue to be a significant Critical Strategic Issue impacting trading partner bottom lines and, therefore, requires significant ongoing strategic focus.

To learn about Pentallect’s Reports/Studies click here