by: Barry Friends | Bob Goldin

February 20, 2018

Sysco, US Foods (USF) and Performance Food Group (PFG) have released their latest quarterly results, and they are, in a word, impressive. The companies are continuing to achieve revenue, case volume and profit growth well in excess of market rates. As a consequence, they are picking up share in a highly competitive, relatively slow growth market. The Big 3 are effectively addressing current market challenges of food cost inflation, increased third party freight and warehouse labor costs, and a growth in lower margin contract business. As is the case with a number of major QSR chains, the Big 3 are reaping the rewards of scale, strategic focus on growth drivers, strong execution, prudent investment, and excellent management.

Sysco, US Foods (USF) and Performance Food Group (PFG) have released their latest quarterly results, and they are, in a word, impressive. The companies are continuing to achieve revenue, case volume and profit growth well in excess of market rates. As a consequence, they are picking up share in a highly competitive, relatively slow growth market. The Big 3 are effectively addressing current market challenges of food cost inflation, increased third party freight and warehouse labor costs, and a growth in lower margin contract business. As is the case with a number of major QSR chains, the Big 3 are reaping the rewards of scale, strategic focus on growth drivers, strong execution, prudent investment, and excellent management.

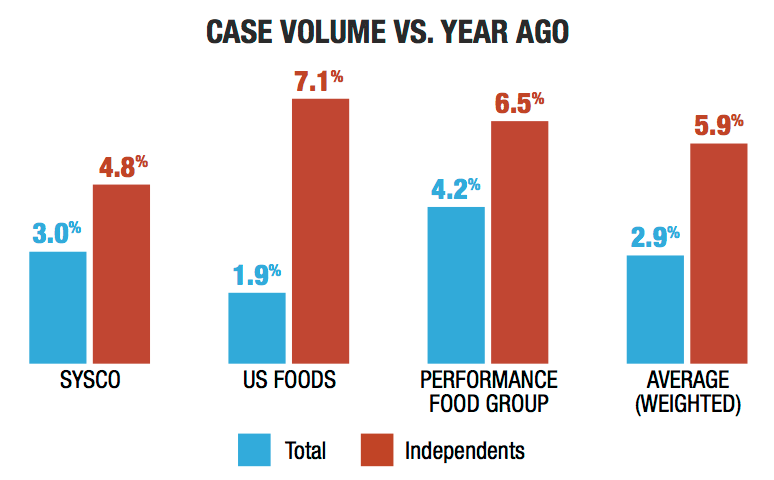

Among other factors, Sysco, USF and PFG point to their growth in independent restaurant case volume and private brands as major contributors to their success. As shown below, the companies experienced an average of 5.9% y-o-y independent case volume growth compared to the independent market average of 2.0% (Pentallect estimate). Their success in penetrating that attractive segment expands their market for their highly profitable brands, thereby creating an unbeatable profit multiplier. As importantly, it also creates a defensible, wide moat for other suppliers seeking to grow with independents. The Big 3’s overall average case volume growth of 2.9% also far exceeds the industry rate of 0.5%.

A few other observations relative to the subject matter:

- All three companies had relatively bullish outlooks for 2018, and cited tax relief as a tailwind. Based largely on favorable economic conditions, Pentallect expects the foodservice industry to grow in the 4% range in 2018, which is a slight improvement over 2017.

- Depending on product mix, the distributors reported food cost inflation of 2.5 – 3.5%.

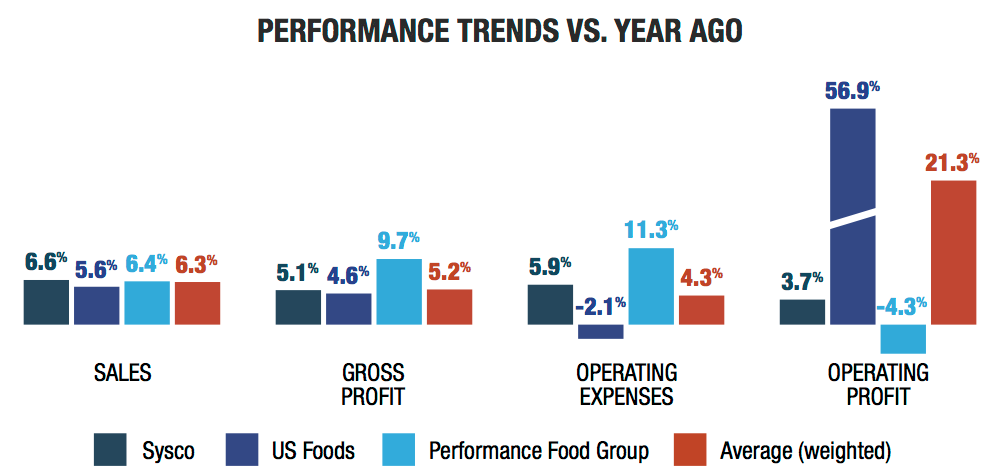

- Each distributor had an increase in gross profit per case, a highly relevant performance indicator.

- Given the Big 3 are growing at 6.3% and the overall market is growing at 3.5%, other distributors (excluding club stores/cash-n-carry, custom distributors and online) have implied growth in the 1.5% range and are likely experiencing volume decline with independents.

- The results of Sysco’s Sygma and PFG’s Customized divisions clearly reflect ongoing softness and challenges in the chain restaurant segment. On a related note, PFG’s Vistar division is a major growth contributor to the company.

The Big 3 are already strong and getting stronger. They appear to be well-positioned for future growth and share gains.