![]()

By: Bob Goldin | Barry Friends

May 8, 2020

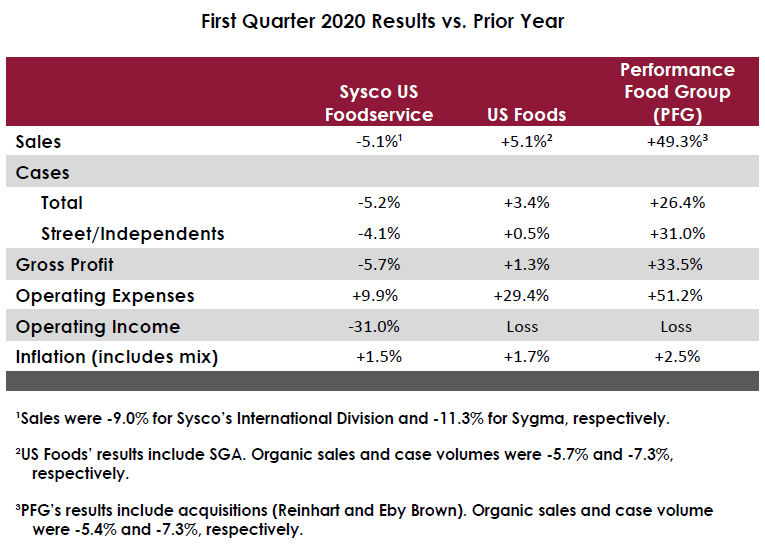

The Covid-19 pandemic caused a dramatic slowdown (and in some segments, a near or total cessation) of virtually all foodservice activity during the last few weeks in March for industry participants of all types and sizes. Even though Sysco, US Foods and PFG have each taken a $100+ million charge to their bad debt reserves, their first 2020 calendar year results only partially reflect the shocking downturn since the pandemic only affected results for the last few weeks of March. While understandably disappointing, these results are almost certainly much better than we can expect for at least for the next several quarters and, more likely, for the next year or more. The upcoming quarters will provide a more complete picture of the pandemic’s destructive impact on these industry leaders and, by logical extension, the industry at large.

Like almost all other industry participants, once the voluntary and mandated industry shutdowns became essentially national in scope, the “Big 3” went into “survival mode.” To their great credit, they took bold and decisive actions to drastically downsize operations, seek alternative revenue streams, and boost liquidity to compensate for the cataclysmic and totally unexpected decline in demand in an industry which is massively and shockingly contracting and which, in our estimation, faces a very protracted, uneven and uncertain recovery. As George Holm, PFG’s CEO stated: “The reduced or discontinued operations of many of our customers will continue to adversely affect demand for our products and services for an inherently uncertain period of time.” Significantly, all three companies have withdrawn future guidance to the investment community. Sysco did warn that they will have an operating loss next quarter.

There is no playbook for crises of this nature and magnitude. “Big 3” company management did, however, pursue similar prudent paths to improve the suddenly diminished prospects for their companies. These actions included:

- Temporary and permanent headcount reductions and hiring freezes. Sysco, for example, reported a 33% reduction in staffing.

- Salary reductions for management level associates

- Issuance of equity and debt instruments

- Drawing down credit lines and ABLs

- Redeploying products and personnel to other channels, most notably retail

- Requesting concessions from suppliers

- Making “on the fly” productivity improvements, e.g., routing

- Reducing and/or deferring capital expenditures

- Halting stock buybacks. Notably, Sysco, a Dividend Aristocrat, has maintained its dividend

- Supporting key operator customers via webinars/training programs, financial means, and related activities

Each company did cite that there has been modest but marked sequential weekly volume upticks in April which they largely attribute to growing consumer acceptance of and greater operator effectiveness in take-out and delivery. As the country slowly and cautiously reopens, foodservice volumes should continue to improve, albeit modestly given the onerous reopening mandates (such as distancing and visit restrictions) and widespread consumer “fear” about returning to many foodservice venues, the “Big 3” stand to benefit. Longer-term, they should be in a very strong position to gain valuable share of a smaller but rebounding market.

The Pentallect team continues to monitor and assess the marketplace and continues to be engaged in post-pandemic planning for their food industry clients. For help in reevaluating, reinventing and reenergizing your go-to-market strategies, please: