Understandably, most large foodservice distributors have been actively rationalizing low volume, high cost-to-serve customers or, at a minimum, imposing stricter requirements (such as higher minimum orders, tighter payment terms, delivery restrictions and/or fuel surcharges) that the referenced customers are often challenged to meet. And when inventories are tight distributors commonly “de-prioritize” smaller customers to ensure they meet service level expectations with large and/or contracted accounts.

Between streamlined distributor product assortments and order fill rate challenges throughout the supply chain, many operators have found themselves needing to scramble, turning to sources they may not historically have relied upon, notably club stores, cash-n-carry, and/or supermarkets. This trend has greatly accelerated during the COVID-19 pandemic.

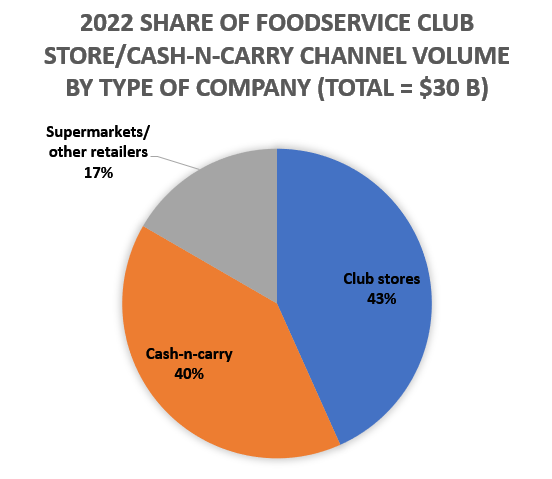

This wholesale channel accounts for $30 billion in volume, a 10% share of the total market but a significantly higher share of its served market.¹ Several of the leading participants – Restaurant Depot, Costco, Sam’s Club, US Foods’ Chef’s Stores (fka Smart Foodservice) and Walmart supercenters each do $1+ billion in foodservice volume, and Gordon Food Service stores is $500+ million. Kroger is entering the “fray” in a more direct fashion with its restaurant supply test in the Dallas/Fort Worth market; the business offers next day free delivery on orders over $250. Significantly, the leading channel participants are extremely well-capitalized companies that are expanding their footprint, modernizing and expanding their customer appeal, and growing their collective share of market.

The channel has been able to capitalize on several factors, some of which are interrelated. We believe these factors will ensure future growth, primarily at the expense of small broadline distributors, while eroding penetration levels at large broadliners.

- A very large customer base, including a vast array of ethnic restaurants

- Increase in unit count/improved accessibility

- Supermarkets have long been “fill-in” venues for certain situations

- Effective foodservice assortment, including ethnic products, perishables, “must have” items and private labels

- A very solid actual (or perceived) value proposition

- Our customer research indicates that operators do not quantify the time it takes to travel to/from and shop at a club store/cash-n-carry

- Relatedly, with distributor cost-to-serve having spiked while service levels suffer, the rationale for “self-serve” is arguably sounder than ever.

- We found that supermarket prices on certain staples like milk and bread are as much as 50% lower than distributor delivered prices

- We also found that operators regard channel pricing as “fair” and “consistent”

- Ability to shop for a wide variety of non-foodservice items (e.g., office supplies, gas), especially at club stores

- Improved in-store experience and merchandising effectiveness

- Favorable economics/business model relative to full-service distributors

- A recovering foodservice market

We are impressed at the staying power and momentum of the club store/cash-n-carry channel. It is uniquely positioned to meet the needs of its customer base, which large distributors are often unwilling or unable to meet. While some channel members will likely expand their delivery and online ordering capabilities and selected supermarket chains will increase their foodservice offerings, the business is fundamentally strong and has lots of growth potential with its current model.

¹Key customers include small independent restaurants and snack stands, caterers, food trucks, vend operators, day care, convenience stores and gas stations, and jobbers.

By: Bob Goldin and Barry Friends